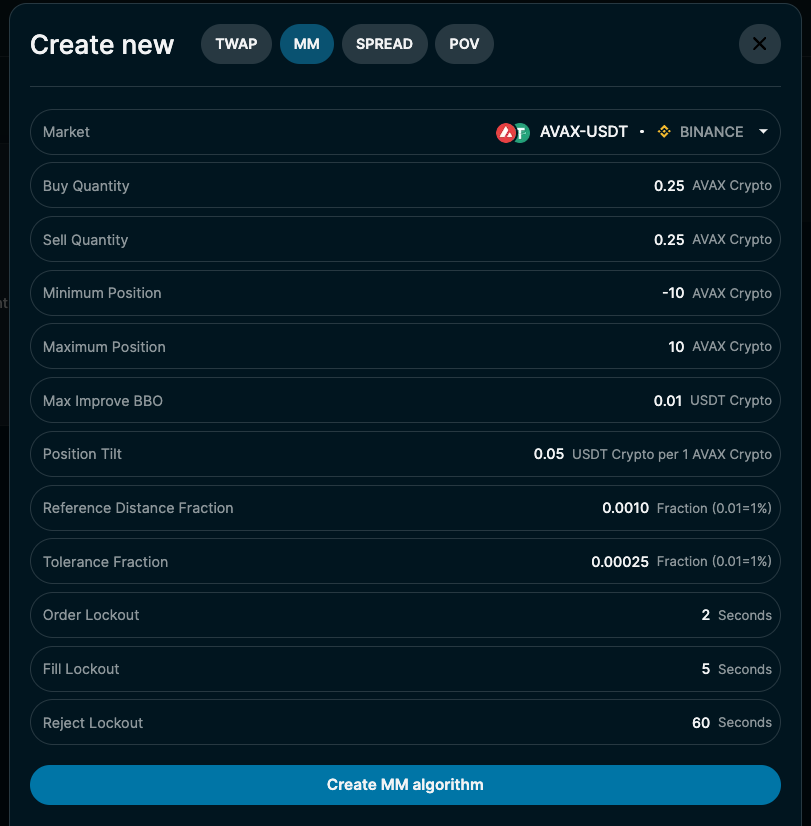

Market Maker (MM) algo in the AVAX/USDT market on Binance. Will send size 0.25 AVAX orders 0.1% away on each side, and will cancel/replace if market moves by 0.025%. As MM algo picks up positions, fade quotes by 0.05 USDT per 1 AVAX position accumulated, and will not send orders to exceed a total position of 10 AVAX.